How much will we need to see us through our retirement years? According to latest research, it’s an eye-watering £420,000.

‘The Cost of Tomorrow’ report, released by the financial planning and investment firm Tilney, has shed some light on the spending habits and aspirations of today’s retirees.

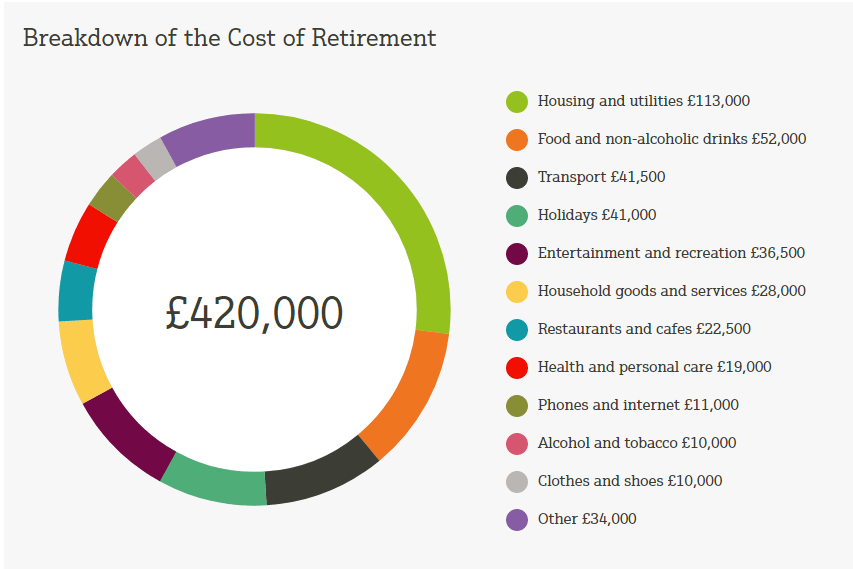

It shows that a typical household aged 65+ can expect the cost of retirement to reach £420,000 – a daunting statistic for some, given how little many of us have set aside for our retirement years.

The ‘sum for fun’

Much of this cost is attributed to housing upkeep (£113,000) and entertainment, for which the over-65s spend £100,000 in retirement.

The £100k ‘sum for fun’ is broken down into £41,000 on holidays, £36,000 on entertainment and recreation, and £22,000 on dining in restaurants and trips to cafés.

Incidentally, the report also reveals that people aged between 45 and 65 underestimate how much they will spend in their retirement years by £100,000.

Perhaps prospective retirees aren’t factoring in the cost of keeping themselves entertained in their golden years?

[donut_chart_cost_retirement]

Top Ten Aspirations for Retirees

- One or more holiday(s) abroad each year 44%

- One or more holiday(s) within the UK each year 43%

- Regularly eating out at restaurants, going to museums, art galleries, cinema or theatre 37%

- Owning a home 34%

- Planning my estate so I can pass money to my children 23%

- Make charitable donations / volunteer 23%

- Take up or continue a sport/hobby 21%

- Update car/motorbike regularly 20%

- Financially supporting children’s / grandchildren’s house purchase 15%

- Move to a part-time job 1%

As we get older our priorities and pastimes naturally evolve. With more freedom and time on our hands in retirement, holidays and entertainment become more of a priority.

Perhaps unsurprisingly, researchers for Tilney’s ‘The Cost of Tomorrow’ report found that having one or more holidays a year dominates the top of the aspirations list.

After holidays came regularly eating out and trips to museums, art galleries and the cinema – a key priority for more than a third of retirees.

With the aspirations of retirees revealed, it’s hardly surprising, that £41,000 – almost 10% of the £420,000 ‘ost of retirement’ – is reserved for holidays.

Property value key to overcoming shortfall?

According to the report, the average household aged 65 – 75 will spend £26,500 every year.

The state pension currently covers £12,719 of this (based on a couple), leaving the average household to find a further £13,781 every year to achieve their retirement aspirations.

According to the Nationwide House Price Index, the average house was worth £206,665 in the first three months of this year – that’s £111,309 more than 15 years ago.

Could prospective retirees be expecting their home’s value to fund their cost of retirement shortfall, perhaps through downsizing or equity release?

For those with considerable years to go until their retirement years, it goes without saying that planning ahead and saving sufficiently can help to ensure a comfortable standard of living.”

For those already in or approaching retirement who are experiencing a shortfall in their finances, the answer may well lie in the value of their property, which could be worth significantly more today than when it was purchased.

Downsizing is a good option for those who are happy to sell their home and move to something smaller, although for many people, this isn’t possible or desired. Equity release on the other hand, could enable them to unlock a lump sum from their home’s value to boost their finances, whilst continuing to own and live in their own home.

With Bower’s help, you can fully understand the advantages and disadvantages of an equity release plan, including how a plan will reduce the amount of inheritance you leave.

Try our calculator to find out how much you could release.