Instantly See How Much Equity You Could Release

If you’re a UK homeowner aged 55 or over, an equity release calculator is the quickest way to understand how much tax‑free cash you could unlock from your home. With just a few basic details, such as your property value, remaining mortgage, and the age of the youngest applicant, you get an instant estimate of how much equity you could release through a lifetime mortgage.

There’s no credit check, no commitment, and no impact on your eligibility for anything. Just a clear, simple estimate of the money tied up in your home.

What the Equity Release Calculator Actually Does

The calculator gives you a personalised estimate of:

- how much tax‑free cash you could release

- how your current property value affects your loan amount

- how your age influences the percentage you can unlock

- how much equity is available after clearing any secured loans

It’s designed to help you understand your position before you speak to an adviser, especially if you’re exploring future financial options, reducing monthly repayments, or simply curious about your property worth.

The Three Details That Shape Your Estimate

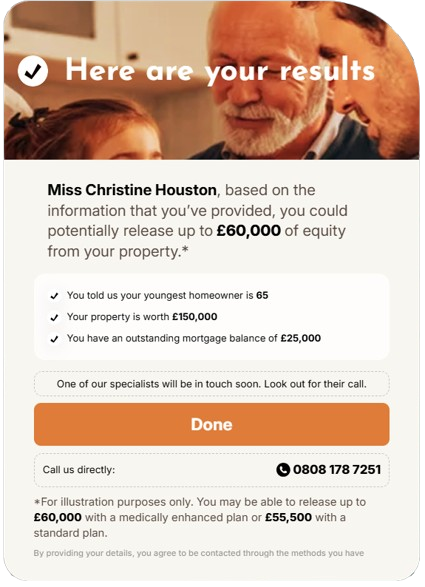

How Much Equity Could You Release?

Most UK homeowners aged 55+ can release 20% to 60% of their property value, depending on:

Age

Property value

Health conditions (which may increase the amount)

Property type

Outstanding mortgage balance

The calculator shows you how much you could release today, based on your current property, not a future property valuation.

Why This Calculator Is Useful

Using an online calculator helps you:

- Understand how much equity is tied up in your home

- See how much you could release tax‑free

- Check whether a lifetime mortgage might be suitable

- Explore options without sharing unnecessary personal details

- Get clarity before speaking to an equity release adviser

- Understand how releasing equity could affect your life finances

It’s the simplest way to get a realistic estimate of the total amount you could unlock.

What Your Estimate Includes

Your personalised estimate will show the maximum loan amount available to you. It is important to remember that any remaining mortgage would need to be repaid. Your estimate will also tell you how your property value, age and any medical conditions may affect the amount you can release. Some plans can be medically underwritten, with some health conditions allowing you to release more funds.

What the Calculator Doesn't Do

The calculator does not:

Confirm eligibility for a specific equity release product

Replace a full property valuation

Assess your tax position

Determine your entitlement to means‑tested benefits

Decide whether equity release is right for your individual circumstances

Those things come later, with independent advice from a specialist.

Understanding Lifetime Mortgages (the Most Common Type of Equity Release)

A lifetime mortgage lets you release equity while continuing to own your home. There are no required monthly repayments unless you choose to make them. Interest can roll up (compound) over time, or you can make optional payments to manage the balance.

Most plans include: No Negative Equity Guarantee, the option to ring‑fence inheritance, flexible drawdown options and the ability to release equity in stages.

Your calculator estimate is based on these lifetime mortgage principles.

How The Calculator Helps You

The calculator helps you understand the numbers, the advice process helps you understand the implications.

How Equity Release Could Affect You

It’s important to understand the wider impact:

- Releasing equity will reduce the value of your estate

- It may affect your entitlement to means‑tested benefits

- Interest is added to the loan amount, which can grow quickly through compound interest

- You will never owe more than your home is worth thanks to the No Negative Equity Guarantee

- You remain the legal owner of your home

Why Start With a Calculator?

A calculator helps you see what’s possible from a lifetime mortgage or home reversion plan by showing how much equity you could release, how your property value influences your borrowing potential, and how much could go towards clearing any remaining mortgage. It also gives you an idea of the tax‑free cash you might access and whether releasing equity could support other goals such as managing debts, funding home improvements, or boosting your retirement income. It’s fast, simple, and completely obligation‑free.

What Happens After You Get Your Estimate

If you choose to share your details, a specialist adviser will talk you through:

- your calculator result

- how much you could release

- how interest works

- how your estate may be affected

- whether a lifetime mortgage, home reversion plan, or alternative is suitable

- whether equity release is the right fit for your individual circumstances

It’s trusted, independent, and whole‑of‑market advice, meaning you’re not tied to any one lender.

Equity Release

Is Equity Release regulated by the Financial Conduct Authority (FCA)?

All equity release plans are regulated by the FCA that are called Lifetime Mortgages or Home Reversion Plans. Bower is also regulated by the FCA to give Equity Release advice as stated on the FCA register under our firm registration number 451607.

Is Equity Release Safe?

However, equity release has safeguards and guarantees in place to help protect those that take out a plan as hundreds of thousands of UK home owners have done for many years.

Bower is also a member of the Equity Release trade body the Equity Release Council.

It is important to understand that entering into a regulated equity release mortgage can reduce the amount of inheritance you leave behind and for some people can affect their eligibility for state welfare and or their tax position.

What is Equity Release?

Equity release is a way to help people over 55 release the money in their home (the equity) without having to move or sell.

The amount of money you can get depends on how much your house is worth, minus any money you still owe on your mortgage.

And it’s good to know that unlike some other companies, we are not tied to any lenders. So, we search the whole of the market to find you the best plan.

Guarantees of Equity Release

The ‘No Negative Equity’ Guarantee which ensures that neither the borrowers nor the family will ever owe more than the value of the property.

As long as you follow the terms and conditions of the loan, you will not lose your home and providing it remains your main residence can live there for as long as you wish.

There will be no debt or money owing left for loved ones to pay.

You can move to another suitable property if desired.

Why Choose Us?

At Bower we are dedicated to providing a reliable, impartial, equity release advice service for our customers. You can feel completely confident and safe in the knowledge that our only priority is giving the right advice for you, even if it is not to take out a plan. We are proud to say that we have received many awards of the past years, voted for by both the public and industry partners. We are authorised and Regulated by the Financial Conduct Authority (FCA) and work closely with the Equity Release Council.

As a member of The Equity Release Council, we recommend the plans that adhere to their code of conduct. In cases where there may be more suitable plans for (whatever reason), we’ll discuss this with you so you can make an informed decision.

IMPORTANT TO KNOW

At Bower Home Finance, we will understand your unique circumstances and advise you to ensure you are receiving the best plan to meet your objectives. There are plans that allow you to make voluntary repayments and move home, subject to lender criteria. However, early repayment charges may apply in certain circumstances.

Bower Home Finance provides independent, impartial whole of market equity release advice with an award-winning customer service experience. Initial advice is provided at no cost to you and without obligation. Only if you choose to proceed and your plan completes, would a typical advice and administration fee of £1,695 be payable.

Equity release requires paying off any existing mortgage. Any money released, plus accrued interest to be repaid upon death, or moving into long-term care. Equity release will reduce the value of your estate and your entitlement to means-tested benefits now or in the future, and impact long-term care funding. If you are considering equity release, we strongly recommend that you read our Equity Release page carefully and talk to one of our specialists before deciding if you wish to proceed.

To find out more about any of the products and the service we provide, please call us on freephone 0800 411 8668, request a call back, email us, or use our live chat on our website.

Please be aware that equity release may involve a home reversion plan or lifetime mortgage which is secured against your property. All features and risks are thoroughly explained in your free personalised illustration.